It’s the first week of the month. Your phone pings with that familiar notification: your salary has been credited. For millions of residents in the UAE, this moment marks the beginning of a mental calculation. You know exactly how much you want to send home, for your parents’ medical bills, your sibling’s tuition, or your own savings.

You enter an amount into an app or hand cash over at a counter, and you see the “final received” figure. It’s a little less than you expected. You’ve planned for this, you’ve earned this. But when the math doesn’t quite add up, it raises one simple, frustrating question: Where did the rest go?

Remittance costs aren’t always obvious, and they don’t work the same for every country. In the UAE ,there are plenty of ways to send money and lots of exchange houses competing for your business. But the true cost of a transfer is often hidden behind technical terms and changing charts.

Many residents feel a sense of “fee fatigue”, the confusion of seeing a low upfront fee only to realize the exchange rate offered is far below the mid-market rate. This lack of transparency makes it difficult to compare services fairly and often results in your family receiving less than you intended.

To get the most value for your salary, you have to stop looking at just the “fee” and start looking at the total cost. Think of every remittance as having three parts:

The UAE is one of the world’s most active remittance hubs, with outward flows reaching over AED 145 billion annually [2]. However, the cost pattern changes significantly depending on the country.

India remains the world’s largest recipient of remittances, crossing the $100 billion mark recently [3]. Because the volume of money moving from the UAE to India is so high, fees are generally the lowest here.

The Trend: Users often make frequent, smaller transfers.

The Catch: Because the market is so competitive, providers often fight on “Zero Fee” marketing. However, the exchange rate fluctuates by the minute. A “free” transfer with a weak rate can actually cost you more than a paid transfer with a premium rate [1].

Pakistan is the second-largest destination for UAE remittances [2].

The Trend: Transfers are often driven by urgent family support, leading to smaller, more frequent amounts.

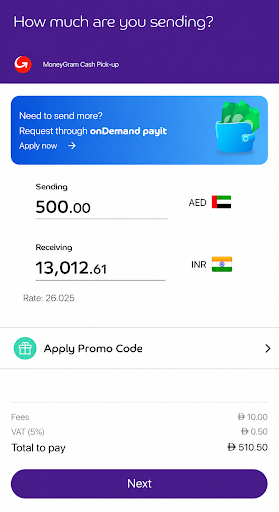

The Catch: Users often face inconsistent “final received” amounts due to bank-side charges in the home country. To maximize value, it helps to use a service that clearly shows the final amount the recipient will receive before you confirm, like remittance on Payit.

For the Filipino community, remittances are often tied to strict monthly deadlines for utility bills and school fees.

The Trend: There is a high demand for “instant” or “same-day” delivery to mobile wallets like GCash or Maya.

The Catch: In many traditional systems, “fast” means “expensive.” Users often pay a premium for speed, which can eat into the total value sent home if they aren’t using a digital-first platform [4].

Millions of residents send money to other vital corridors like Egypt, Bangladesh, Sri Lanka, and Nepal. This is where the “one-size-fits-all” approach to remittance completely breaks down.

The most important lesson for these corridors is that a service that is the cheapest for India might be the most expensive for Egypt. Fees vary based on:

A small difference in fees or a slightly lower exchange rate might seem like “pocket change” in a single transaction. But for a professional sending money home every month, these costs add up.

Over a year, losing AED 30–50 per month to hidden margins means your family receives up to AED 600 less annually. That is money that could have covered a month of groceries, a utility bill, or an emergency fund. When you lack visibility on these costs, it doesn’t just affect your wallet, it affects your family’s budget planning and your trust in the system.

You don’t need to be a financial expert to send money smarter. Use these four practical tips to ensure more of your hard-earned money reaches home:

This is where Payit changes the experience. As a digital wallet powered by First Abu Dhabi Bank (FAB), Payit was built to solve the “hidden cost” problem.

With Payit, the confusion is removed. Before you even click “confirm,” you see:

Sending money home doesn’t have to feel like a gamble. You aren’t doing anything wrong; the system has just been hard to see through for a long time. With a better understanding of how fees and rates interact, and by using tools that prioritize transparency over hype, you can take back control of your finances.

The right tool doesn’t just move your money; it protects its value. Use the right platform, check the math, and make sure that the people who matter most receive exactly what you intended for them.

[2] Payments and Commerce Market Intelligence

[3] World Migration Report 2026 – “Top 10 Remittance Receiving Countries